Fixed Deposits Deliver -2.66% Returns Over a Decade; Dividend Growth Strategy Surpasses ₹20 Lakh with 110%+ Growth

New actuarial research reveals that the annual 30% tax drag on Indian Fixed Deposits resulted in a mathematical loss against 5.5% inflation, whereas the Nifty Dividend Opportunities 50 successfully absorbed new 12.5% LTCG tax to create real wealth.

Saharanpur, Uttar Pradesh Apr 21, 2026 (EMWNews.com) – Independent finance publication Financexaditya has released a 10-year actuarial analysis comparing the actual wealth creation of Indian Bank Fixed Deposits against the Nifty Dividend Opportunities 50 Total Return Index (TRI).

The data covers the period from January 1, 2016, to January 1, 2026. It adjusts gross returns for a 30% tax bracket, an average annual inflation rate of 5.5%, and the newly updated 12.5% Long-Term Capital Gains (LTCG) tax.

The mathematical results show a strict wealth gap for Indian investors allocating capital to fixed income.

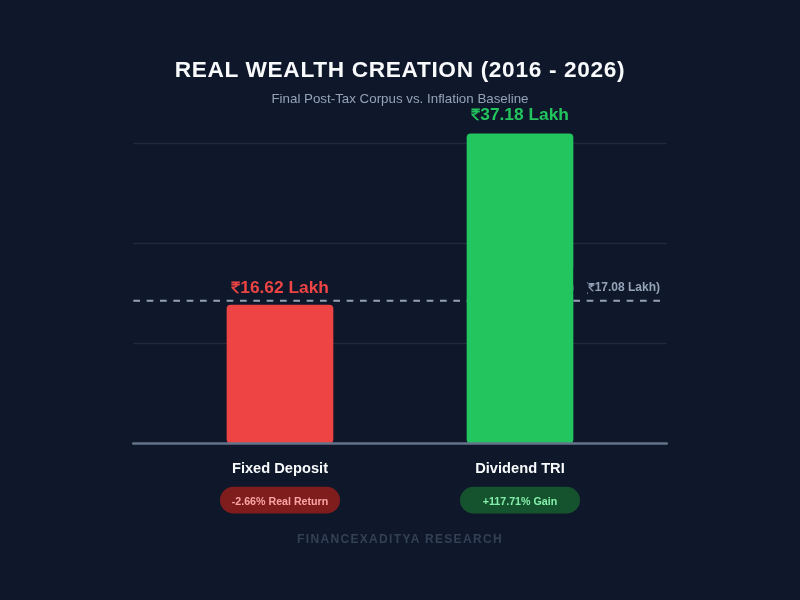

According to the analysis, a 10 Lakh investment in a standard 10-year Bank FD booked at 7.25% in 2016 generated a final post-tax maturity of 16,62,648. However, due to annual tax on interest at the 30% slab, the effective post-tax yield fell to 5.21%.

When measured against the 5.5% inflation baseline of 17,08,144 required to maintain original purchasing power, the FD resulted in a net loss of 45,496. This represents a real return of -2.66% over the decade.

In contrast, an identical 10 Lakh allocated to the Nifty Dividend Opportunities 50 TRI compounded at 15.12% over the same period. Because capital gains in this structure are taxed only upon withdrawal, the capital is compounded without annual tax interruption.

After applying the 12.5% LTCG tax, minus the 1.25 Lakh exemption, the final post-tax maturity reached 37,18,895. This outpaced inflation, generating a real wealth surplus of 2,010,751, representing a +117.71% gain.

“The annual 30% tax drag on fixed deposits mathematically destroys purchasing power over a decade,” says Aditya Gaur, founder of Financexaditya. “The data proves that delaying the tax burden through a dividend-growth ETF, even after paying the new 12.5% LTCG, is mathematically superior for long-term wealth.”

The complete research data, including methodology, tax calculations, and year-by-year actuarial tables, is available at Financexaditya.

Source :Financexaditya

This article was originally published by EMWNews. Read the original article here.

FREE Money In 2024 The Average Family Will Receive $22,967 On Gov’t Grants If They Apply.

There’s nothing complicated about it, Get Your FREE Money!

NO CREDIT Check – Bankruptcy OK – Apply Online

https://GrantsAvailable.com

[youtube https://www.youtube.com/watch?v=a0g8UEDB47Y?si=cKR-DuN-n7I_rB4d&w=560&h=315]